Key Highlights

- Blockchain is a decentralized digital ledger that records transactions securely.

- Every transaction is stored in blocks connected through cryptography.

- Blockchain eliminates the need for a central authority in many applications.

- Bitcoin introduced blockchain to the world, but the technology has far broader uses.

- Industries including finance, healthcare, logistics, gaming, and AI are adopting blockchain solutions.

Introduction

If you’ve spent any time reading about cryptocurrency, Bitcoin, NFTs, Web3, or decentralized finance (DeFi), you’ve likely encountered the term blockchain.

But exactly what is blockchain?

Why do experts call it one of the most revolutionary technologies since the internet?

And why are governments, banks, startups, and major technology companies investing billions into blockchain development?

In simple terms, blockchain is a secure digital record-keeping system that allows information to be stored and shared across a network without relying on a central authority.

Think of it as a digital notebook shared among thousands of computers worldwide. Once information is written into this notebook, it becomes extremely difficult to alter or delete.

This guide explains blockchain technology in beginner-friendly language, covering how it works, why it matters, its advantages, risks, and future potential.

What Is Blockchain?

Blockchain is a distributed digital ledger that records transactions across multiple computers.

Instead of storing information in one central database, blockchain distributes copies of the ledger across thousands of network participants.

Each transaction is grouped into a block.

When a block becomes full, it is linked to the previous block using cryptographic technology.

This creates a chain of blocks—hence the name blockchain.

Because every participant maintains a copy of the ledger, altering historical records becomes extremely difficult.

Simple Example

Imagine a classroom where every student owns an identical notebook.

Whenever a new transaction occurs, every notebook gets updated simultaneously.

If one student tries to change an old entry, all the other notebooks reveal the discrepancy immediately.

Blockchain works similarly but on a global digital scale.

Why Was Blockchain Created?

Before blockchain, digital systems relied heavily on trusted intermediaries such as:

- Banks

- Governments

- Payment processors

- Corporations

These institutions maintain databases and verify transactions.

The challenge is that centralized databases can be:

- Hacked

- Manipulated

- Corrupted

- Mismanaged

Blockchain introduced a way to verify and store information without requiring a central authority.

The concept gained worldwide attention in 2009 when Bitcoin launched as the first successful blockchain-based cryptocurrency.

How Does Blockchain Work?

Understanding blockchain becomes easier when broken into simple steps.

Step 1: A Transaction Is Initiated

A user sends information across the network.

Examples include:

- Sending Bitcoin

- Recording ownership

- Signing a digital contract

- Storing data

Step 2: The Transaction Is Broadcast

The transaction is shared with network participants called nodes.

Nodes are computers connected to the blockchain.

Step 3: Validation Process

Network nodes verify the transaction according to predefined rules.

Validation may involve:

- Checking balances

- Confirming ownership

- Preventing double spending

Step 4: Block Creation

Verified transactions are grouped together into a block.

Step 5: Cryptographic Linking

The new block receives a unique cryptographic signature called a hash.

The hash connects the new block to the previous block.

Step 6: Block Added to Chain

After consensus is reached, the block becomes part of the blockchain permanently.

The updated ledger is shared across the network.

Key Components of Blockchain

Blocks

Blocks contain transaction data.

Each block includes:

- Transaction details

- Timestamp

- Previous block hash

- Current block hash

Hashes

A hash is a unique digital fingerprint.

Even a tiny change in data creates an entirely different hash.

Nodes

Nodes are computers that maintain blockchain copies and validate transactions.

Consensus Mechanisms

Consensus mechanisms ensure agreement across the network.

Popular methods include:

Proof of Work (PoW)

Used by Bitcoin.

Miners solve complex mathematical puzzles to validate transactions.

Proof of Stake (PoS)

Used by many modern blockchains.

Validators lock cryptocurrency as collateral to secure the network.

Types of Blockchain

Public Blockchain

Anyone can join and participate.

Examples:

- Bitcoin

- Ethereum

Private Blockchain

Access is restricted to authorized participants.

Often used by businesses.

Consortium Blockchain

Controlled by multiple organizations.

Common in enterprise environments.

Hybrid Blockchain

Combines features of public and private blockchains.

Blockchain vs Traditional Databases

| Feature | Blockchain | Traditional Database |

| Control | Decentralized | Centralized |

| Transparency | High | Limited |

| Security | Very High | Moderate |

| Data Changes | Difficult | Easy |

| Trust Model | Trustless | Requires Trust |

| Failure Risk | Low | Higher |

Why Is Blockchain Secure?

Blockchain security comes from several layers.

Cryptography

Data is encrypted using advanced mathematical techniques.

Decentralization

Information exists across many computers.

Immutability

Once recorded, data is extremely difficult to modify.

Consensus Validation

Network participants verify transactions collectively.

This combination makes blockchain highly resistant to fraud and cyberattacks.

Real-World Uses of Blockchain

Many people think blockchain is only about cryptocurrency.

In reality, blockchain powers numerous industries.

Cryptocurrency

Bitcoin and thousands of digital assets rely on blockchain.

Banking and Finance

Blockchain enables:

- Faster payments

- Cross-border transfers

- Reduced transaction costs

Supply Chain Management

Companies track products from manufacturing to delivery.

Healthcare

Patient records can be stored securely while improving accessibility.

Real Estate

Property ownership records can be verified digitally.

Gaming

Players can truly own in-game assets through blockchain.

NFTs

Non-fungible tokens use blockchain to prove digital ownership.

Voting Systems

Blockchain may improve election transparency and reduce fraud.

Digital Identity

Secure identity verification becomes possible without centralized databases.

Artificial Intelligence

Blockchain can improve AI transparency, security, and data integrity.

Understanding Smart Contracts

Smart contracts are self-executing agreements stored on a blockchain.

The contract automatically performs actions when specific conditions are met.

Example

A freelance designer completes a project.

Once approved:

- Payment is automatically released.

- No middleman is required.

Smart contracts reduce:

- Costs

- Delays

- Human errors

Ethereum popularized smart contract technology and remains a leading platform for decentralized applications.

What Makes Blockchain Revolutionary?

Blockchain solves one of the internet’s biggest challenges:

Digital Trust

Traditionally, trust depends on intermediaries.

Examples:

- Banks verify payments.

- Governments verify identities.

- Companies verify ownership.

Blockchain replaces institutional trust with mathematical verification.

This shift enables entirely new business models and decentralized ecosystems.

Benefits

Enhanced Security

Blockchain’s cryptographic structure makes unauthorized modifications extremely difficult.

Transparency

Transactions can be publicly verified.

Decentralization

No single entity controls the network.

Reduced Costs

Fewer intermediaries mean lower operational expenses.

Faster Transactions

Many blockchain networks process transactions quickly.

Better Traceability

Assets can be tracked throughout their lifecycle.

Improved Data Integrity

Records become tamper-resistant and verifiable.

Global Accessibility

Anyone with internet access can participate.

Challenges / Risks

Despite its advantages, blockchain is not perfect.

Scalability Issues

Some networks struggle with high transaction volumes.

Energy Consumption

Proof-of-Work systems require substantial electricity.

Regulatory Uncertainty

Governments continue developing blockchain regulations.

User Errors

Lost private keys can result in permanent asset loss.

Security Vulnerabilities

Applications built on blockchain can contain bugs.

Adoption Challenges

Many businesses face integration difficulties.

Market Volatility

Blockchain-related assets often experience significant price fluctuations.

Expert Insights

Industry experts increasingly view blockchain as foundational infrastructure for the digital economy.

According to technology researchers, blockchain’s greatest value may not come from cryptocurrency alone but from creating transparent, verifiable, and decentralized systems.

Major organizations continue investing in blockchain solutions for:

- Payments

- Identity management

- Logistics

- Healthcare

- Financial services

- Artificial intelligence

As infrastructure improves, blockchain adoption is expected to accelerate across industries.

Future Outlook

The future of blockchain appears promising.

Several trends are shaping the next phase of development:

Web3 Growth

Decentralized internet applications continue expanding.

Institutional Adoption

Banks and corporations increasingly explore blockchain technology.

Tokenization

Real-world assets are being represented digitally.

AI and Blockchain Integration

Combining AI with blockchain may improve transparency and trust.

Government Initiatives

Many countries are exploring blockchain-based systems and digital currencies.

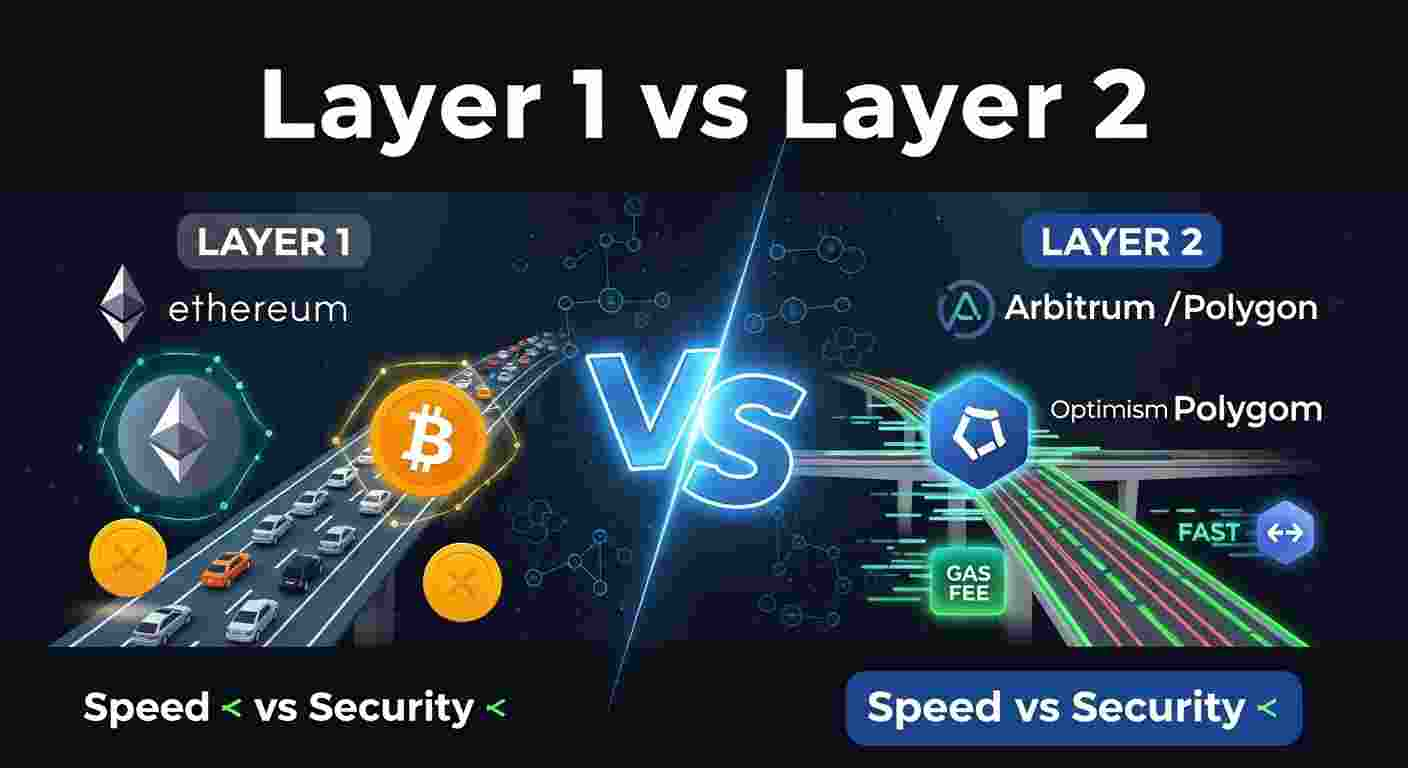

Improved Scalability

Layer-2 networks and new consensus mechanisms aim to increase transaction capacity.

Over the next decade, blockchain could become as essential as the internet itself.

Conclusion

Blockchain is far more than the technology behind Bitcoin.

It represents a new way of storing, sharing, and verifying information without relying on centralized authorities.

By combining decentralization, cryptography, transparency, and consensus mechanisms, blockchain creates secure and trustworthy digital systems.

Whether you’re interested in cryptocurrency, DeFi, NFTs, Web3, AI, or enterprise technology, understanding blockchain provides a strong foundation for navigating the future digital economy.

As adoption continues to grow worldwide, blockchain is likely to influence how we transact, communicate, manage data, and establish trust in the digital age.

Frequently Asked Questions

1. What is blockchain in simple words?

Blockchain is a digital ledger that stores information securely across multiple computers instead of one central location.

2. Who invented blockchain?

Blockchain technology was popularized by the anonymous creator of Bitcoin, known as Satoshi Nakamoto.

3. Is blockchain the same as Bitcoin?

No. Bitcoin is a cryptocurrency, while blockchain is the technology that powers it.

4. Can blockchain be hacked?

The blockchain itself is highly secure, but applications, wallets, or exchanges connected to it can sometimes be compromised.

5. What are smart contracts?

Smart contracts are self-executing agreements that automatically perform actions when conditions are met.

6. Why is blockchain important?

Blockchain improves security, transparency, efficiency, and trust in digital systems.

7. What industries use blockchain?

Finance, healthcare, logistics, gaming, real estate, AI, government services, and many others.

8. Is blockchain the future?

Many experts believe blockchain will become a core technology supporting the next generation of internet services and digital infrastructure.

Leave a Reply